Lecture 9 - Short-term Financial Planning

Short-term Financing Sources

In our previous lecture, we saw that firm’s short-term capital needs can arise due to from temporary and permanent needs, according to (Berk and DeMarzo 2019):

Permanent needs relate, in general, to working capital investment that will be necessary throughout the lifetime of a firm (or a project)

Temporary needs, on the other hand, arise due to seasonalities, positive and negative cash-flow shocks

Ways for financing short-term working capital needs range from a variety of sources:

- Bank Financing

- Commercial Papers

- Secured Financing

- Bank Financing

In what follows, we’ll details the main aspects of each financing source

Bank Financing

- One of the primary sources of short-term financing, especially for small businesses, is the commercial bank. Some types include:

Single Payment Loan: pay interest on the loan and pay back the principal in one lump sum at the end of the loan. Can have a fixed or variable interest rate structure

Credit lines: case where a bank agrees to lend a firm any amount up to a stated maximum

- Generally used for seasonal needs

- Commited versus uncommited

- Revolving Credit lines

Bridge Loans: used to “bridge the gap” until a firm can obtain long-term financing

- Watch-out for stipulations and fees! These increase the effective interest rate: origination fees, commitment fees, compensating balance requirements etc

Commitment Fee - Example

Various loan fees charged by banks affect the effective interest rate that the borrower pays

For example, the commitment fee associated with a committed line of credit increases the effective cost of the loan to the firm. The “fee” can really be considered an interest charge under another name.

Example: Suppose that a firm has negotiated a committed line of credit with a stated maximum of $1 million and an interest rate of 10% ( EAR) with a bank. The commitment fee is 0.5% (EAR). At the beginning of the year, the firm borrows $800,000. It then repays this loan at the end of the year, leaving $200,000 unused for the rest of the year. The total cost of the loan is:

(+) Interest on borrowed funds: $800,000 \(\times\) 10% = 80,000

(+) Commitment on unused portion: $200,000 \(\times\) 0.5% = 1,000

(=) Total Cost = 81,000

(=) Effective Interest Rate, inclusive of Fees: (881,000/800,000)-1=10.125%

Loan Origination Fee - Example

- Another common type of fee is a loan origination fee, which a bank charges to cover credit checks and legal fees:

- The firm pays the fee when the loan is initiated; like a discount loan, it reduces the amount of usable proceeds that the firm receives.

- And like the commitment fee, it is effectively an additional interest charge.

Example: assume that it is offered a $500,000 loan for 3 months at an annual percentage rate (APR) of 12%. This loan has a loan origination fee of 1% charged on the principal.

- The amount of the loan origination fee is \(1\% \times 500,000 = 5,000\)

- The actual amount borrowed is \(500,000-5,000=495,000\)

- The interest rate is charged on the total, not the discounted value: $500,000 \(\times\) (3%) = \(15,000\)

- Therefore, the annual effective interest rate is 515,000/495,000 - 1 = 4.04%

Compensating Balance Requirements - Example

- Regardless of the loan structure, the bank may include a compensating balance requirement in the loan agreement that reduces the usable loan proceeds

Example: assume that, in the previous example, rather than charging a loan origination fee, the bank requires that the firm keep an amount equal to 10% of the loan principal in a non-interest-bearing account with the bank as long as the loan remains outstanding

- If that is the case, then the requirement amount is 10% \(\times\) 500,000 = 50,000

- Thus, the firm has only $450,000 of the loan proceeds actually available for use, although it must pay interest on the full loan amount

- Therefore, the actual three-month interest rate paid is:

\[ \small \dfrac{(500,000 + 15,000 -50,000)}{(500,000-50,000)}-1 = \dfrac{465,000}{450,000}-1=3.33\% \]

Other thoughts on bank financing

The three examples outlined before are situations where banks charge extra costs from customers. Why these costs arise?

- Legal requirement checks

- Credit analysis

- Need to reduce the risk of the amount to recover in case of default

Some firms (in general, smaller and newer firms) may not have other options rather than a bank. But that does not mean that bank financing will always lead to higher implied costs:

- Long-standing client-bank relationships can convey information about the credit quality of the firm and reduce interest rates

- Some banks specialize in certain activities (e.g, Rabobank) to better manage risks and understand client’s inherent risks

There can also be subsidized operations for certain activities. See, for example, the role of BNDES in Brazil

Commercial Papers

Commercial paper is a short-term, unsecured debt used by large corporations

The interest on commercial paper is typically paid by selling it at an initial discount

In Brazil, also referred to as nota promisória comercial: the goal is to target short-term financing

Example: suppose that a firm issues three-month commercial paper with a $100,000 face value and receives $98,000. What is the annual effective rate is the firm paying for its funds?

- Using our present value formula to analyze the full 3-period interest rate, we have:

\[ FV=PV\times(1+i)^n \rightarrow i=\dfrac{100,000}{98,000}-1 =2.04\% \]

Commercial Papers in the U.S. at the onset of the COVID-19 pandemic:

The Covid-19 crisis severely disrupted the functioning of short-term US dollar funding markets, in particular the commercial paper and certificate of deposit segments1

- Investors become reluctant or unable to provide new credit or roll over existing ones…

- Issuers faced challenges in obtaining short-term financing at reasonable rates…

- Fligh to safety: investors withdrawn money from riskier assets to move it to safer affects…

- This movement cascaded over to fund managers in which, pressured by withdraws, had to fire-sale assets at higher discounts to make liquidity

- Contagion Effect: due to these accumulated effects, other markets such as the stock market experienced unusually high volatility during the period

Secured Financing

Businesses can also obtain short-term financing by using secured loans, which are loans collateralized with short-term assets

Commercial banks, finance companies, and factorings, which are firms that purchase the receivables of other companies, are the most common sources for secured short-term loans:

- Using Accounts Receivable as collateral

- Using Inventories as collateral

- PPE as collateral

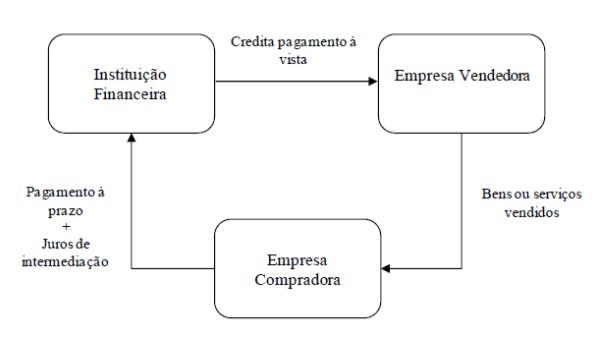

Secured Financing in Brazil - Desconto de Duplicatas

- This type of operation is, in essence, a loan from the bank to the firm that is secured by accounts receivable:

- The firm sells its products to customers, which will pay in a determined date

- The bank then extends a loan to the firm, that will receive a discounted value at the present time

- The bank will then receive the original amount in the accounts receivable

All else held constant, this operation has a lower cost than a simple loan, as accounts receivables are backing up the loan and reducing the bank’s risk

It is important to note that the bank does not bear the risk of not being paid - the obligation from the firm to repay the bank persists

Secured Financing in Brazil - Vendor

A vendor operation occurs when a firm sells a product to a client, which will pay with a predefined date, and transfers the credit function to the bank

The firm bears the responsibility of paying the amount due if the client does not pay

Secured Financing in Brazil - Compor

On the other hand, a compor operation occurs when the customer pays the firm upfront, and the bank provides credit to the customer for a specific commercial operation

The customer contracts the credit directly with the bank, and thus the firm does not bear any risk in the event of non-payment

Institutional stability and investor protection

- Whenever property rights and contract-enforcement are put in risk, lenders adjust interest rates to cope with the expected risk

- For example, as seizing collateral may involve a lot of bureaucracy, banks adjust the interest rates for some specific credit contracts

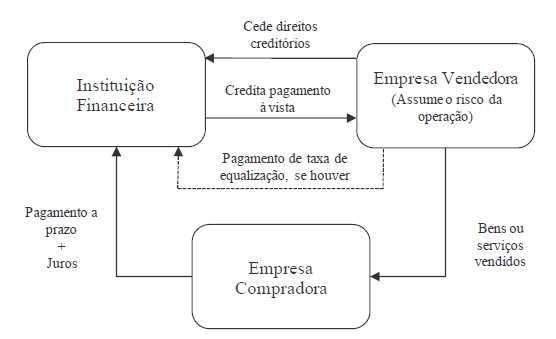

Factorings

Similar to a discount operation, the key difference reside in the risk in the event of non-payment:

On the one hand, in discount operations (desconto de duplicatas), a financial institution provides cash-in-advance to a firm using its accounts receivable as a collateral, with the firm bearing the risk of non-payment from its customers

On the other hand, in a factoring operation, a commercial partner acquires the credit and bears the full responsibility of its risk, providing the firm with cash-in-advance

Factoring firms are not financial institutions, but rather commercial partners (sociedade mercantil), which can be financed through equity or bank financing, but it cannot issue publicly shares

Although it does not involve merely a financial service, involves a series of continuous commercial services, such as credit analysis and management, risk management, payables and receivables management, and buying the firm’s account’s receivables and bearing its risk

Fundos de Investimento em Direito Creditório - FIDCS

A common way to organize resources to finance short-term mismatches is through the use of a FIDC1, which is similar to discount operations and factoring

How it works: suppose that a firm sells its products to customers with a 90-days payment, and it needs money today to finance its operations:

- A FIDC collects money from investors aiming to be exposed to credit operations

- A FIDC then buys several credit obligations, in the same way that a factoring firm does, and bears the risk of the operation

- Ultimately, the shareholders of the FIDC are the ones bearing the risk in the event of non-payment by the firm’s clients

- Key benefit: FIDCs do not need to concentrate risk in only one type of credit operation/customer

References

![]()

Presented by Lucas S. Macoris